The Growth Watchlist: March Edition

5 Brands in Decline — And What Summer Is Trying to Tell You

Summer is when brands reveal the truth. Backyards. Road trips. Ballparks. Streaming nights.

The highest-frequency, highest-emotion consumption moments of the year. And this year, the signal is unmistakable:

Consumers didn’t disappear.

They just chose differently.

Across five categories— from hot dogs to gasoline— the pattern is the same:

The brands that lost didn’t lose demand.

They lost relevance in how demand shows up today.

Here’s what CMOs should be paying attention to.

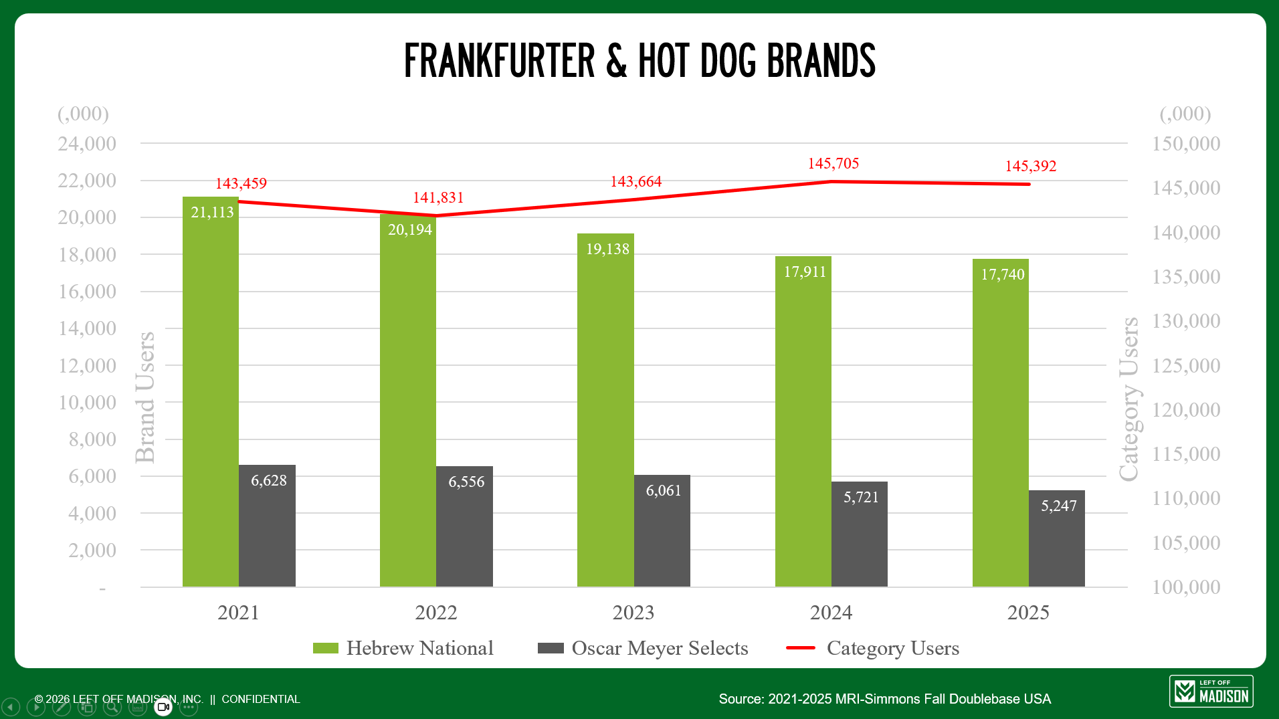

1. Hebrew National — When Trust Stops Converting

Hebrew National, owned by ConAgra, lost more than 3 million users in a category that’s flat to slightly growing. Meanwhile, Nathan's Famous surged (Owned by Smithfield Foods under WH Group).

This isn’t about hot dogs. It’s about what “quality” means now.

Hebrew National was built on:

Trust

Standards

“Answering to a higher authority”

But today:

Quality is assumed

Premium is redefined (cleaner, sourced, modern)

Culture drives choice (nostalgia, spectacle, identity)

Nathan’s sells:

Experience

Ritual

Summer culture

Hebrew National sells:

Assurance

That used to close the sale. Now it just gets you considered.

Diagnosis: A classic “stuck in the middle” brand— not premium enough, not cheap enough, not culturally loud enough.

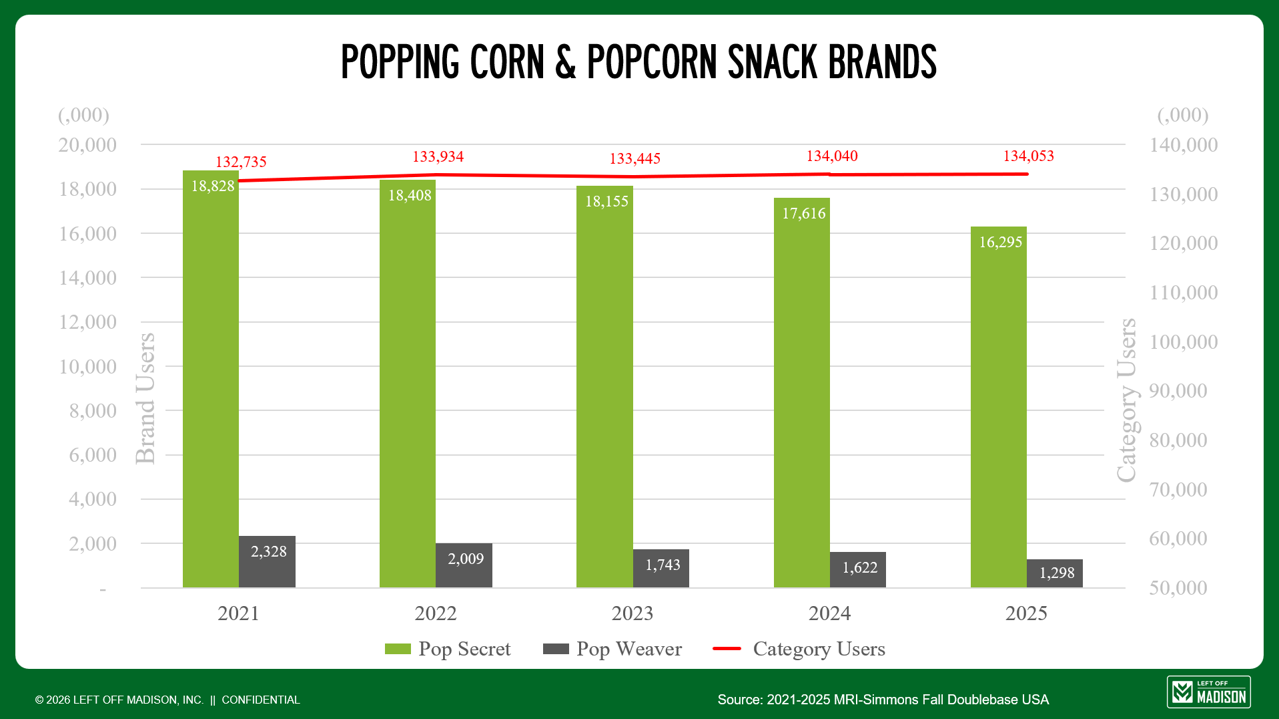

2. Pop Secret — When Occasion Loses to Habit

Pop Secret (owned by Our Home) lost 2.5 million users in a flat category. Meanwhile, SkinnyPop exploded (+4.3MM users; owned by The Hershey Co.).

Pop Secret owns:

Movie night

Butter

The microwave

But the category moved from:

Occasion → Everyday behavior

SkinnyPop sells:

Permission

Simplicity

Identity (“I snack smarter”)

Pop Secret still signals:

Effort (microwave)

Indulgence

A single moment (the couch)

Meanwhile, consumers snack:

At their desk

In the car

After workouts

Late at night

Habit beats occasion.

Diagnosis: A brand locked in a shrinking usage moment while competitors expanded frequency.

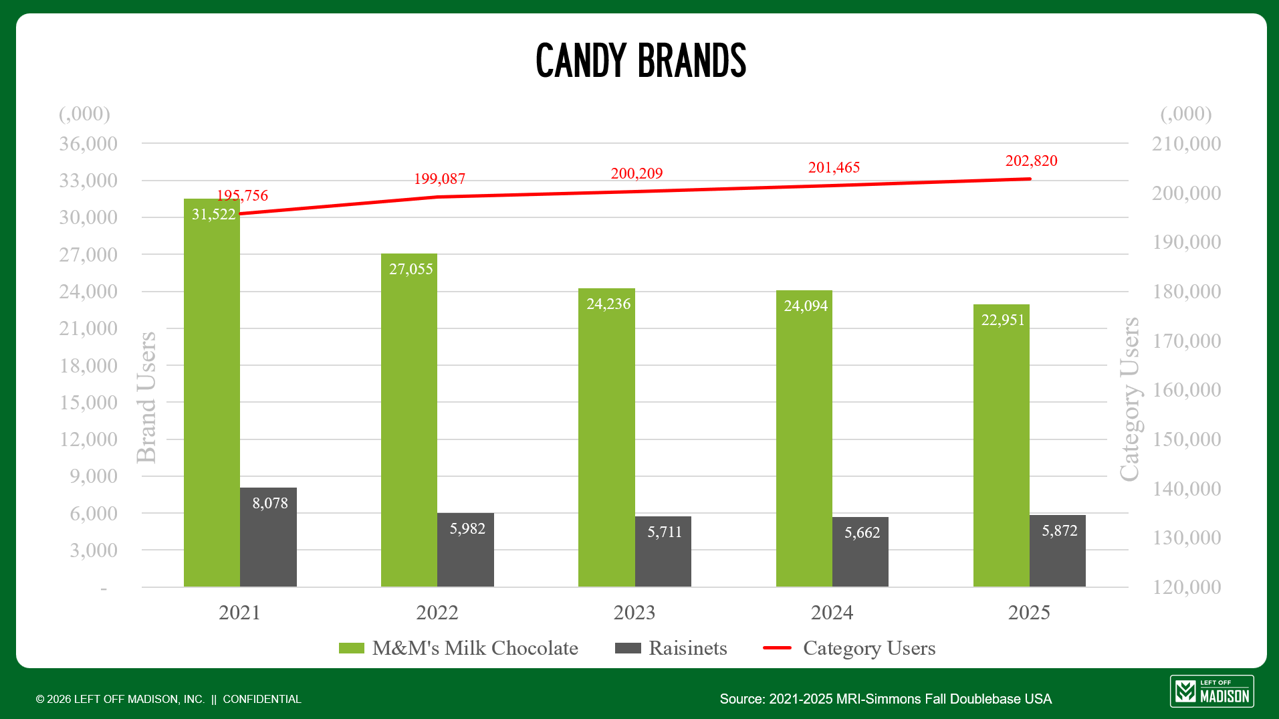

3. M&M’s Milk Chocolate — When Familiar Becomes Forgettable

M&M’s (owned by Mars, Inc.) lost 8.5 million users in a growing category (+7MM users). Heavy usage is up +22%.

That’s the paradox:

People are eating more candy. Just not this one.

Growth went to brands like:

Sour Patch Kids (+32%) - owned by Mondelēz International

Nerds (+79%) - owned by Ferrara Candy Co.

Kit Kat (+4.2MM users) - owned by Nestlé

What do they all have in common?

Sensory intensity

Novelty

Shareability

Cultural energy

Candy is no longer just a product. It’s content.

M&M’s Milk Chocolate is:

Reliable

Consistent

Iconic

And increasingly…

Expected

Diagnosis: Over-reliance on legacy equity in a category driven by novelty and stimulation.

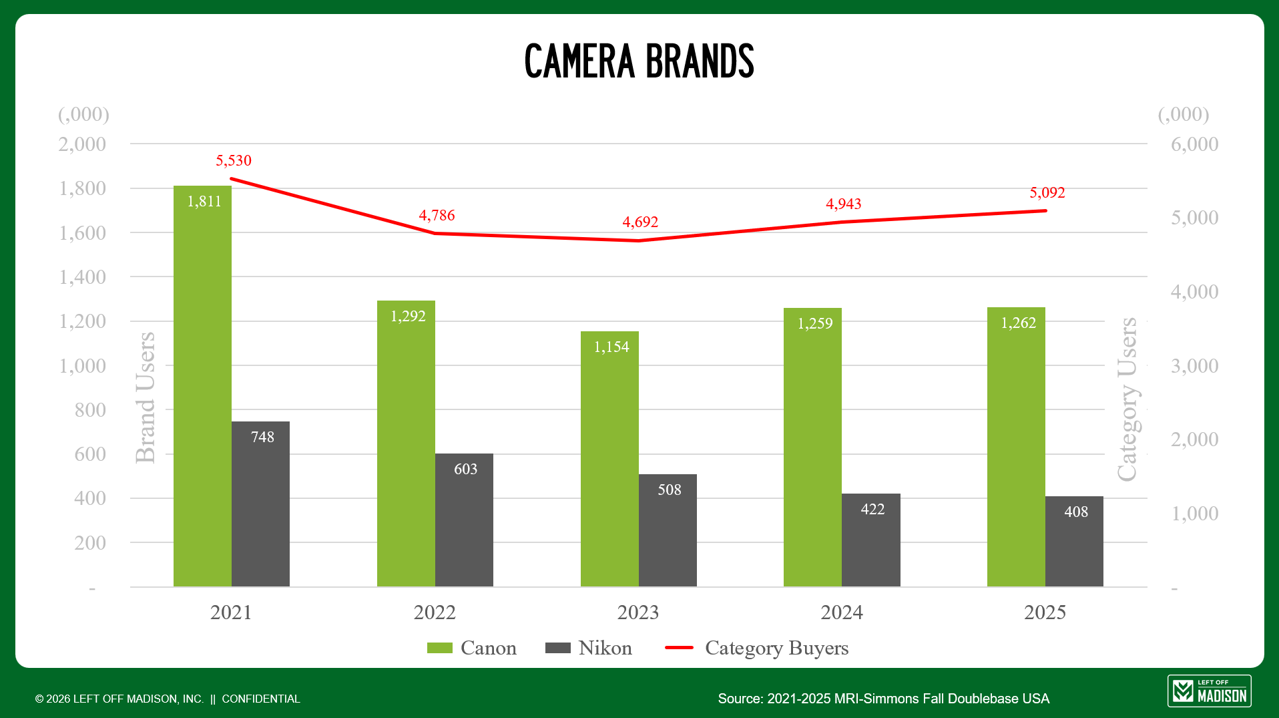

4. Canon — When the Middle Disappears

Canon (-30%) and Nikon (-45%) lost buyers in a declining category (-8%). But here’s the real shift:

Professionals: +12%

Advanced amateurs: -11% (-1.7MM people)

The middle is collapsing. And that’s exactly where these brands built their dominance.

Meanwhile, LUMIX (owned by Panasonic) grew +70%.

Why? Because the definition of a camera changed.

From:

Taking photos

To:

Creating content

Today’s buyer:

Shoots video

Publishes instantly

Thinks in audience, not albums

Smartphones own convenience. So cameras must own capability + creator relevance.

LUMIX leaned into:

Hybrid shooting

Video-first features

Creator workflows

Canon and Nikon stayed anchored in:

Photography heritage

Diagnosis: A legacy stronghold in a segment (advanced amateurs) that is disappearing.

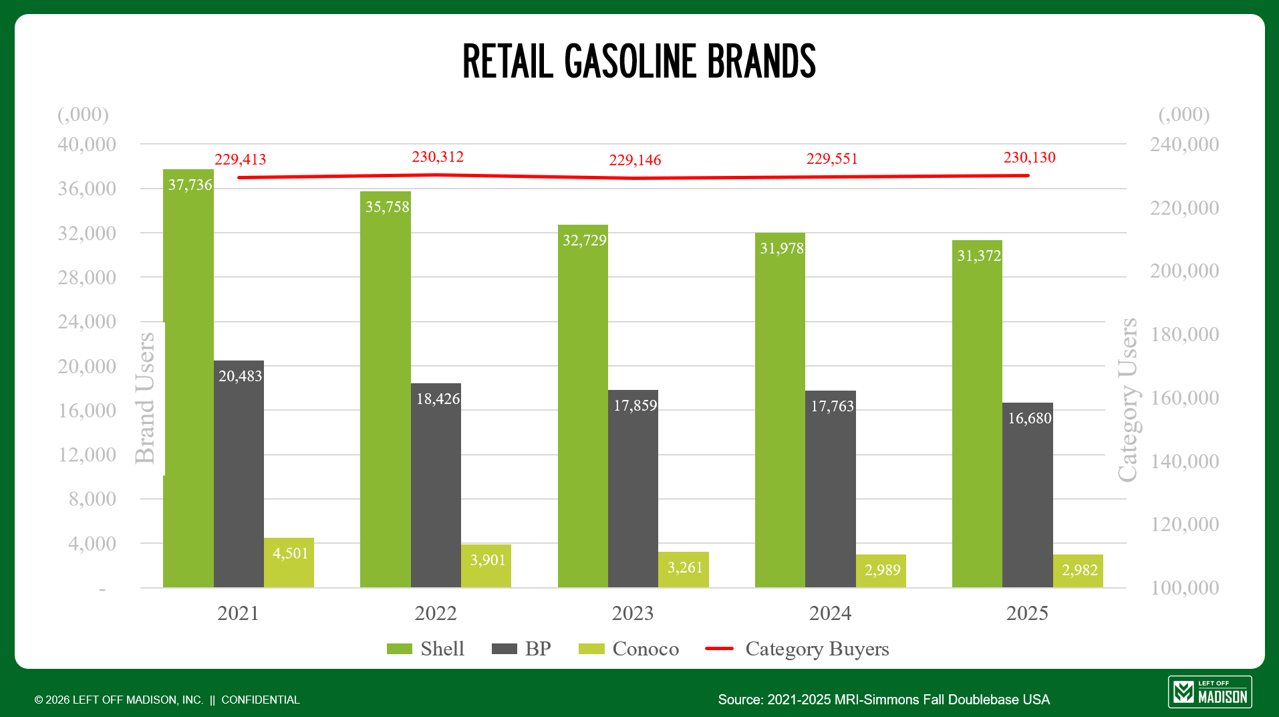

5. Shell — When Brand Loses to Math

Shell lost 7.5 million users. BP and Conoco followed. Meanwhile:

Costco: +4.9MM users

Walmart: +2.3MM

7-Eleven: +1.5MM

Category demand is flat. But heavy users are up +23%.

That means: The most valuable customers are buying more—and optimizing harder. Gas has become:

A price decision

A proximity decision

An ecosystem decision

Not a brand decision.

Costco sells:

Smart savings

Walmart sells:

Everyday value

7-Eleven sells:

Time

Shell sells:

Gasoline

Diagnosis: In a commodity category, if you don’t create value beyond price, you lose to those who do.

The Pattern Across All Five

Different categories. Same story. Across summer’s most visible consumption moments:

Backyard grilling

Snacking

Travel

Entertainment

Content creation

Consumers are shifting toward:

1. From Trust → Relevance

Trust is expected.

Relevance drives choice.

2. From Occasion → Frequency

Winning brands show up more often, not just in big moments.

3. From Product → Identity

People don’t just buy what something is.

They buy what it says about them.

4. From Familiarity → Stimulation

Safe doesn’t win anymore.

Interesting does.

5. From Brand → System

Increasingly, brands win when they are part of:

A lifestyle

An ecosystem

A daily behavior

The Real Takeaway for CMOs

None of these brands failed because their products got worse. They failed because:

The context around them changed faster than they did.

And in every case:

The warning signs were visible early

The category data was clear

The shifts were behavioral, not sudden

The Opportunity (For Those Willing to Act)

Every one of these declines is reversible.

But not with:

Incremental innovation

More media spend

Better optimization

It requires:

Reframing the role of the brand

Redefining the value exchange

Re-entering culture with intent

Because the brands that win next summer won’t just be:

Seen

Or remembered

They’ll be:

Chosen—more often, more easily, and for better reasons.

Final Word

Summer doesn’t create brand problems. It exposes them. And right now, it’s exposing a simple truth:

Growth doesn’t come from doing more.

It comes from becoming more relevant to how people live today.